Starmaker - Opera's 19.35% Investee

This is part 1 of 3 part series on detailed analysis of Opera’s minority investments to show how undervalued these stakes are on Opera’s books and how market is not realizing the significant upsides these minority stake offer to Opera’s ADS.

Introduction

Starmaker, of which Opera owns 19.35% after a $30M investment in 2018, is a fast-growing technology-driven social media company focused on music and entertainment, with a user base in emerging markets such as India, Indonesia and the Middle East.

Starmaker has grown revenue from $12M in 2018, to $29M in 2019(136% YoY Growth) , to $90M(210% YoY growth) in 2020. Opera reported that starmaker was doing close to $180M run rate in Q1 2021.

Starmaker is also profitable with 2020 net income of $13M ( 255% YoY Growth).

On Opera's books, Opera has valued its 19.35% stake in starmaker at $55M, which significantly undervalues this growth and offers a significant upside to Opera based on its sum of part valuation.

StarMaker Financials

Star Maker Sensor Tower stats

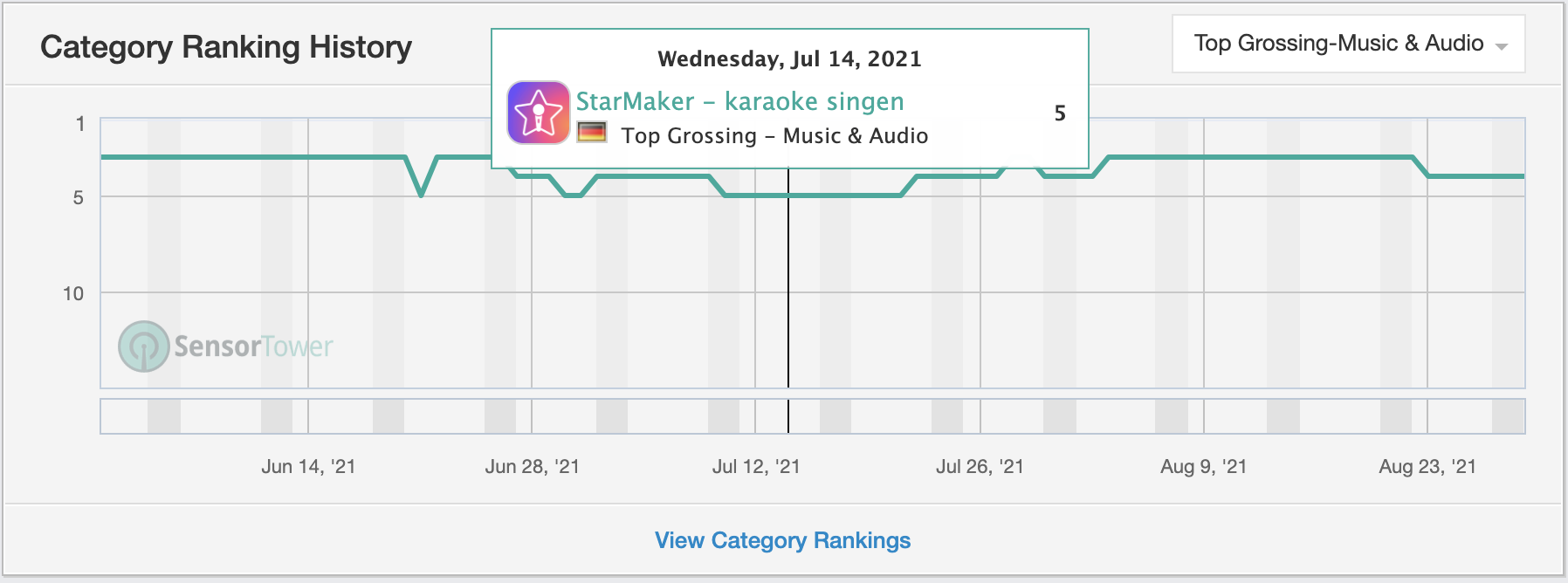

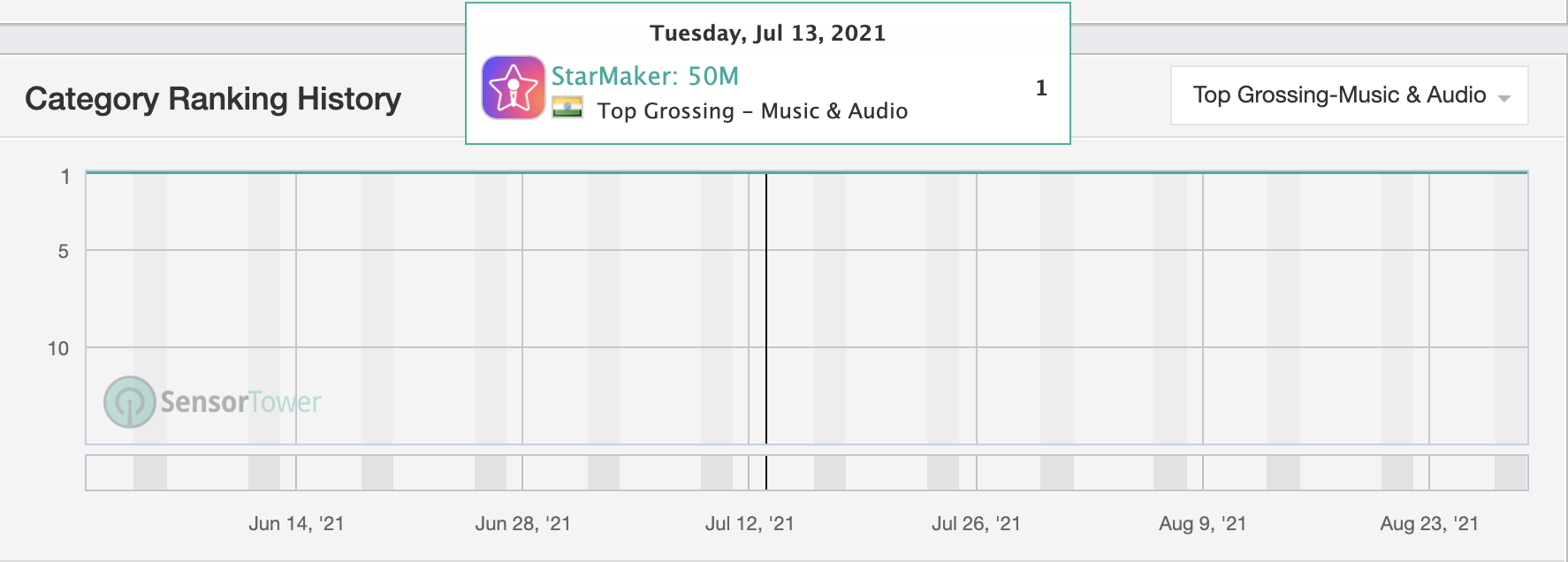

Sensor tower stats for play stores shows that Starmaker is both top 5 music and audio app and top 5 grossing music and audio app in top western and emerging markets.

More recently, starmaker has brought in more social elements to its app and has been seeing a strong growth in FY ‘21.

Following is the sensor tower google play store data for starmaker in major western and emerging markets which shows that star maker has not faded away after the covid related bump in downloads and popularity.

US

France

Germany

UK

India

Indonesia

Philippines

UAE

Brazil

How to Value Starmaker since it is not public

The closest comparison is with Smule which also operates apps similar to starmaker and caters to similar music and karaoke audiences.

Smule last raised $54M funding in 2017 at $604M valuation when it was doing about $100M revenue in 2016.

Quote from the article -- Reuters reports that the round valued the company at $604 million and that an IPO is in the planning stages. Last year Smule revenue grew 54% to $101 million, monthly active users increased by 52% to 52 million and subscribers by 100%.

The mobile infrastructure in emerging markets has significantly improved since 2017 and provides many opportunities to better monetize the free users as observed by facebook, Snapchat and tiktok.

If Smule got 6x revenue multiple for 54% YoY growth back in 2017 when the mobile user monetization was in its infancy in emerging markets , it is not unreasonable to give starmaker a 20-40 revenue multiple, when it is growing at 100+% YoY and is profitable. Pinterest and snap all commanded similar revenue multiples when they were growing at 100%+ YoY.

With ~$180M run rate in Q1 '21 and continuation of growth, I am forecasting FY '21 revenue of $226M for starmaker. At 20x revenue multiple, Starmaker is worth $4.5B and at 40x revenue multiple, starmaker is worth $9B.

Even if one wants to conservatively value starmaker, given the EM exposure and potential competition from tiktok and other big giants, It is still fair to value starmaker at, at least 10-16x revenue multiple on $226M of FY'21 revenue for that 100%+ growth.

Hey Bryce,

what do you think of the sale of stake in Starmaker? And at the sale price?

Overall, Starmaker is valued at apparently around 400 million. You had estimated a significantly higher value (4.5-9 billion). I personally think you were way too optimistic here (as with Nanobank), but even by my guess Starmaker should be worth a lot more right now. About 1.2-1.5 billion.

Also that the buyer is Kunlun Tech shows again that Zhou Yahui practices nepotism here and is not interested in increasing shareholder value for investors. Are you still comfortable with your investment? An exit may also be imminent at Opay (again at a too low price).

What else do you think Opera plans to do with all that cash? Do you think there is a major project coming up? If you add the approx. 130 million from the sale of Nanobank and the 85 million from the sale of Starmaker to the 180 million in cash at the moment, you are at around 400 million. Opera is currently only worth 600 million. On paper, this is starting to look like a really good deal. Especially if my thesis proves true and we go a whole lot deeper in the overall market in the coming weeks.

Besides Yahui, the old rat, has to convert Opera into a private company before, so that the shareholders get nothing.